SMM, December 27:

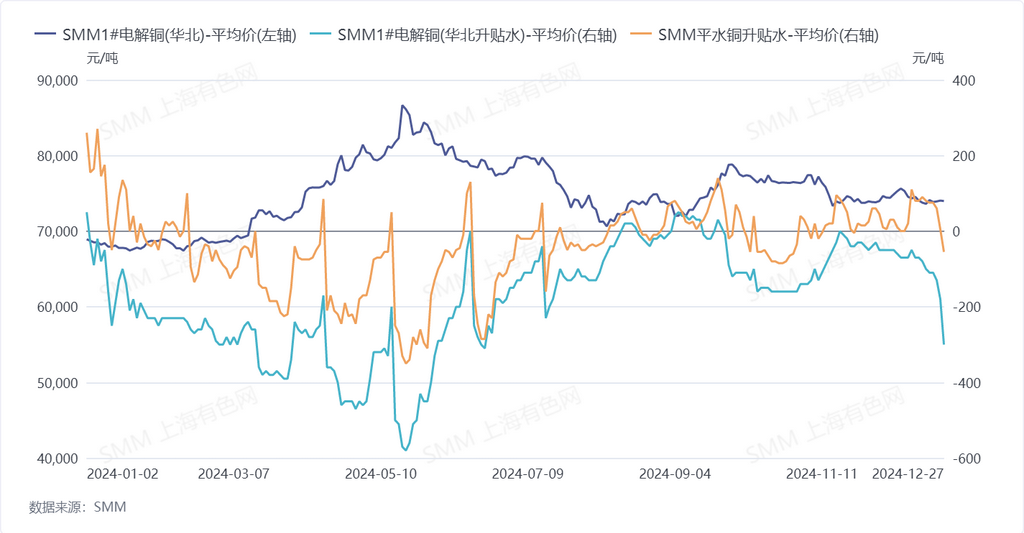

According to SMM prices, as of December 27, 2024, the monthly average spot premiums/discounts for SMM #1 copper cathode in north China in December 2024 stood at a discount of 88 yuan/mt, down 20 yuan/mt MoM from November's average discount of 68 yuan/mt. The annual average spot premiums/discounts for SMM #1 copper cathode in north China in 2024 recorded a discount of 179 yuan/mt, down 117 yuan/mt YoY from 2023's discount of 62 yuan/mt.

The spot premiums/discounts in north China weakened MoM in December, mainly due to seasonal consumption weakness in the north as year-end approached. Additionally, downstream sectors faced funding constraints, especially in the final trading days, when upstream producers began to clear inventory by lowering prices, causing spot premiums/discounts to drop below a discount of 300 yuan/mt at one point.

For the full year of 2024, as the demand in the north China market showed a high correlation with copper prices, spot premiums/discounts were sluggish in H1 2024, primarily due to a surge in copper prices that significantly suppressed consumption. The lowest monthly average discount of the year, 580 yuan/mt, was recorded in late May. With the rapid pullback in copper prices in H2, demand was significantly boosted as downstream enterprises rushed to meet annual targets. Additionally, in Q3, major smelters in north China underwent maintenance, reducing production and tightening supply, which drove up spot premiums/discounts. By early September, the monthly average spot premiums/discounts reached a high of a premium of 50 yuan/mt.

As 2025 approaches, construction projects in the north are expected to be affected by winter weather, and downstream sectors will gradually halt operations before the Chinese New Year, leading to overall weak market demand. Meanwhile, the annual long-term contract negotiation period for copper cathode in the north China market is later than in other regions, with 2025 long-term contract pricing set to begin after the Chinese New Year. However, judging from this year's average spot premiums/discounts, the outlook for 2025 long-term contracts remains pessimistic.